Media and the Press have highlighted significant movements within the energy markets over recent weeks. This reporting has not been sensational when compared to the rapidity and range of pricing swings observable in the Electricity Commercial Market. Renewable Partnerships felt that it might be helpful to share some more background information.

There are a number of elements to the current ‘perfect storm’.

In N Ireland there has been historically a very close correlation between the price of Gas and Electricity. Albeit that there is some pressure on this link it is still material.

At a Global Level there has been significant shortfall of supply against demand. There are some medium-long term factors that impact this:

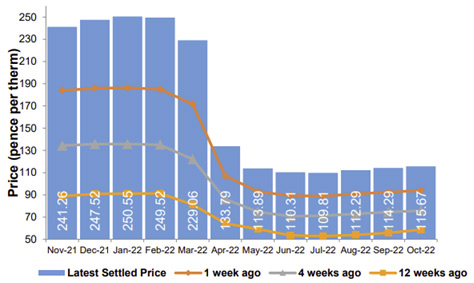

A normal Fixed-Price Contract will be a blend of forward buying choices throughout the duration of a contract. What this chart, supplied by SSE, shows is that gas to be delivered in (for example) Feb 2022 has risen in cost from £0.90/ therm 12 weeks ago to almost £2.50/ therm.

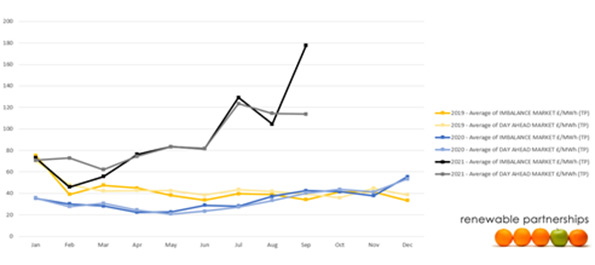

Similarly the £ per MW cost of electricity (spot price – imbalance) has risen. The September 2019 Imbalance price of £35.20 has risen to £177.83 – translated as the energy-only component of a unit of electricity rising from 3.52 pence to 17.78 pence – ignoring pass-through costs.

Energy Suppliers and Large Volume users commonly ‘buy-forward’ on the market. Essentially they contract-now for energy to be delivered at points in the future. When a business ‘fixes’ a price for a year, the supplier should have transacted within the market for energy to be supplied at Month 1, Month 2 and so on. Forward purchasing can be commonly bought as much as five years ahead:

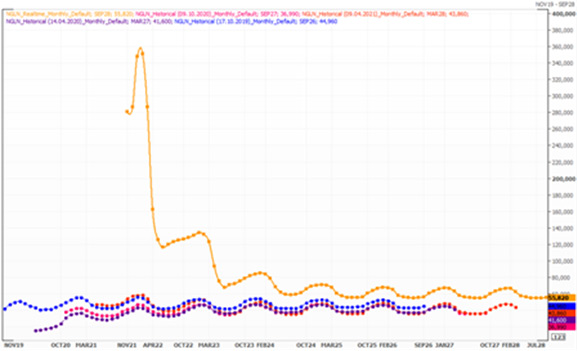

Traders are currently transacting at a very high prices in the 5 years Forwards Market. This pricing is determined by actual commercial trades, not sentiment

The current forward markets suggest that gas will fall to a rate in Summer that exceeds any previous Winter and that little respite will occurs until Summer 2022. The ongoing years continue to show higher that historic price levels.

The Market tells us that prices will remain high for the next 18-24 months although probably not at the current extreme levels. Forward buying shows transactions staying at a level above all previous years – so high energy prices will remain a feature.

The extreme fluctuations have forced all (bar 1) suppliers to shut-up shop – virtually no new business has been written until mid October.

The next ‘Basket Buying’ opportunity via Renewable Partnerships is going to open up in February and we anticipate significant interest in both our 18 and 36 month offers. If no deflation takes place in the market then clients will see increases between 60% and 100% on their current bills.

The current market is historically unprecedented. We hope that inflation falls back. However as advisors and brokers we feel that it is important that you are fully appraised of the potential impact of the market and that budgetary forecasts may need to be amended.