The current volatility in the electricity market has largely been driven by the unpredictability in the Gas market where a mis-match of demand and immediate supply had caused unprecedented price spikes. Rising carbon prices payable by generators burning fossil fuels is also an increasingly important factor.

During Q3 and Q4 of 2021 in particular these price spikes have been exacerbated with the All-Irish Market experiencing the lowest wind speeds since 1962, along with Generation outages such as Whitegate Power Station near Cork (now offline until February 2022). Wind generated power is unpredictable and in itself can be responsible for some very big swings in spot electricity prices.

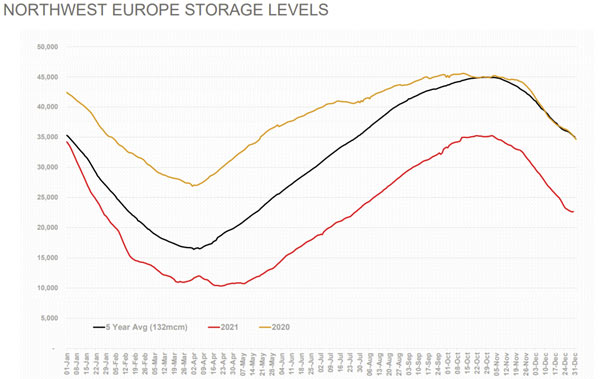

The end-user effect of price spikes would normally be ameliorated via the depletion of national reserves. These normally grow in Summer and reduce in Winter but are currently at historically low levels, in part to a late Winter in Asia 2020. Low European and UK Gas reserves also compound the gas volatility currently observed and are currently at 51% of capacity when they would normally be 76% of capacity in January.

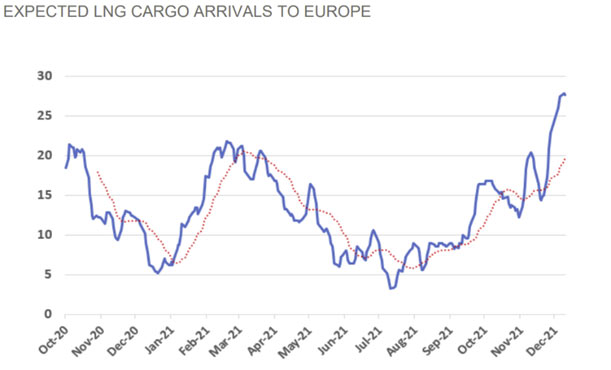

The Pre-Christmas Gas price drop was partly driven by the arrival of Gas-Cargo Shipping into NW Europe in late December 2021.

China, S Korea, Japan and Brazil were competing for these shipments and the spike in Summer 2022 forward Pricing that is apparent at the time of writing (see below) suggests that the relief won’t be extended.

Normally gas producers increase supply into a high-priced market to exploit the revenue and profit opportunity. Supplies from Russia at present do not reflect this pattern and (red line) supply has been below historical norms. Since inflation occurs at the ‘margin’, this reduction has proved highly destabilising.

Demand in Asia, especially China, is growing. Power outages in NW China have stimulated the construction of new Electricity Generation plants, all supplied by Fossil Fuels, especially Coal but also Gas. Albeit that gas supply into Europe is increasing, global demand is also increasing, and shipping cargos will be bid for competitively. Rebuilding storage will be slow and expensive.

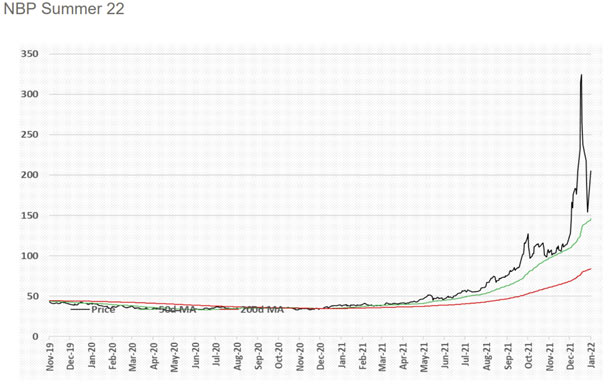

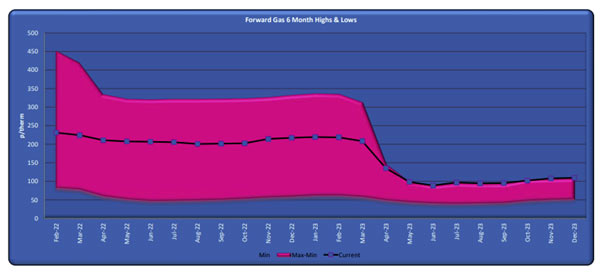

Place this alongside unreliable supply from Russia and French Nuclear issues, then Power markets have become increasingly expensive. The example Forward Graph below shows high Gas pricing through 2022 with a stable but high level maintained in 2023. Gas powered generators are the dominant ‘price setters’ for Power prices in the all-Island electricity market.

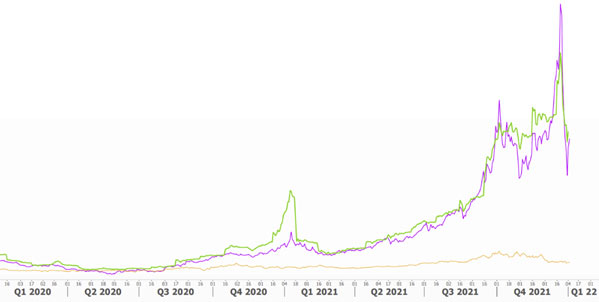

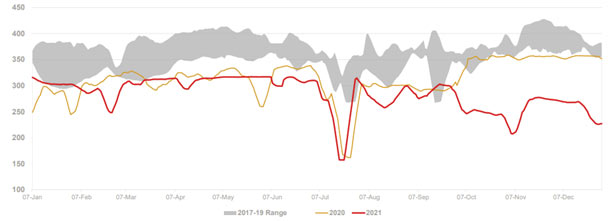

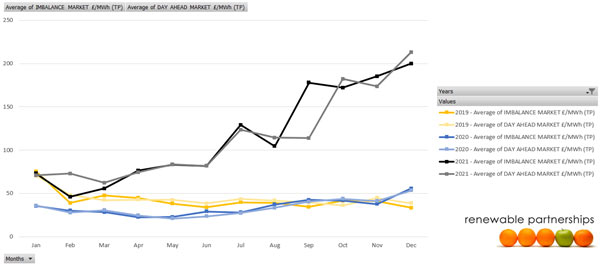

The graph below shows the raw energy costs for electricity in N Ireland in £ and expressed as the arithmetic average of half hourly actual market prices without Use of Sytems loss-adjustment increases. Two markets are available to Suppliers – Imbalance Market (IM) and Day Ahead (DA). There is no such thing as a ‘Wholesale’ Market. The prices shown are a function of a variety of generation sources, most relevantly gas and wind, but also reflect generation and inter-connector issues.

For our larger clients we are recommending a Hedge/Flex product which for example allows you to fix 25%-50%-75%-100% of your volume in a range of 3-36 months. Should prices rise then 'at least we have locked away 50%'. If prices fall then ‘at least we only fixed 50%’. For an increasing large component of your overhead, risk management is especially important.

For very large clients we provide risk managed hedging (fix and unfix) within fully flexible contracts that extend up to 3 years ahead.

For our smaller clients, presently, we are recommending that you adopt a contract which starts variable but that can be ‘fixed’ at any stage of the 24-36 month duration. The importance of budget certainty is unique to each organisation and action can be taken depending on the trade-off of predictability and value.

We look forward to presenting these options to each of our clients as renewal deadlines come into view.

If you are currently in an expensive contract please email us at the address below. We will endeavour to visit you to explain the options available to you and review the best way to navigate the current tempestuous market conditions.